Analysis of Prescription Drug Prices in Hospitals

Escalating healthcare spending and growing concern over medical debt have intensified calls for greater transparency in U.S. hospital pricing. In response, federal policymakers implemented the Hospital Price Transparency Rule — requiring hospitals to publicly disclose detailed “standard charges,” including gross charges, discounted cash prices, and insurer-specific negotiated rates. The intent behind this policy is clear: to reduce long-standing information barriers, empower patients and purchasers, and promote more competitive healthcare markets.

This paper, and its accompanying hospitaldrugprices.org dashboard, presents one of the most comprehensive examinations to date of hospital drug pricing data disclosed under these rules. Using machine-readable files published by hospitals nationwide — and consolidated through the Patient Rights Advocate repository — we analyzed more than 1,300 hospital chargemaster files for prescription drug pricing patterns across facilities, payers, and regions. We applied a structured data-normalization process to extract drug-related records, focusing on high-expenditure pharmaceuticals central to cancer care and multiple sclerosis treatment.

Our findings highlight significant progress in the availability of hospital price data but also reveal persistent shortcomings in data quality, completeness, and comparability. While 93% of downloaded files adhered to CMS’ required format, only 62% of files ultimately contained usable pricing for the most common and expensive medications used in hospital settings — a gap that reflects the distinction between “in-form” compliance (posting a file) and “in-spirit” compliance (providing complete, accurate price information). What is more, the analysis reveals that substantial variation persists not only across hospitals but within hospitals, where prices for the same drug can differ ten-fold or more depending on payer contracts and billing unit inconsistencies.

The analysis reveals that hospitals typically report one gross charge and one cash price, but they yield multiple negotiated rates for each drug. While there is often consistency in list prices (i.e., gross charge or discounted cash price) presented to payers and patients, the majority of a hospital's patients — those with insurance — face a confusing array of potential prices. When the same drug or healthcare service can have a dozen different prices from the same provider on the same day, it becomes difficult to argue that there is a defined price for that product or service at that location.

When we analyzed the aggregate trend of a hospital’s gross charge for a prescription drug service relative to the same hospital’s cash discount (i.e., the price for those without insurance), we found that approximately one-quarter of the time, no discount from the inflated gross price was offered. Furthermore, in half of the analyzed instances, the cash discount was only 30% or less off the gross charge.

In comparison, most negotiated rates by insurers appeared to average around 40% off gross charges (average 39.7%; median 40%). Thus, a patient would generally expect to receive a 10% lower price for a prescription drug from a hospital through their insurer compared to relying solely on the cash discounted price. However, these averages obscure a wide range of negotiated rates.

Despite a highly consolidated U.S. health insurance industry, hospital negotiated rates were sometimes as little as 10% discount of the gross charge (~7% of observations). Indeed, in several cases, uninsured cash prices were lower than insurer-negotiated rates, contradicting expectations and underscoring the limitations of traditional assumptions about insurance “discounts.” In other words, the diverse set of observed cash discounts and negotiated rates means that patients have little hope of effectively shopping the healthcare market today (and may miss opportunities to save on healthcare expenditures, such as by forgoing the use of insurance and paying a cash rate).

Disease-specific analyses further reveal wide spreads between hospital list prices, commercial negotiated amounts, and drug acquisition benchmarks such as Medicare’s Average Sales Price (ASP). In all instances of the five studied drugs in this report, it was uncommon for the negotiated rate to be below the manufacturer list price (i.e., wholesale acquisition cost [WAC]) or benchmark Medicare payment rate [ASP + 6%]). The data indicate that insurers often pay substantial markups above Medicare payments, highlighting considerable hospital profits for these drugs — often exceeding those of the drug manufacturers themselves.

The interquartile range of hospital negotiated prices for these five drugs, expressed as a percentage of ASP + 6%, shows staggering price variations. Calculated exclusively from values within this range to avoid outliers, the results reveal differences in negotiated rates of more than fourfold from high to low in some instances. We believe ASP + 6% is a conservative estimate of hospitals’ acquisition costs, suggesting our analysis likely underestimates hospital markups and margins, especially since we did not factor in 340B discounts. Notably, over half of outpatient drug sales are to hospitals participating in the 340B program, where prices average approximately 22.5% lower than ASP, according to the Medicare Payment Advisory Commission (MedPAC).

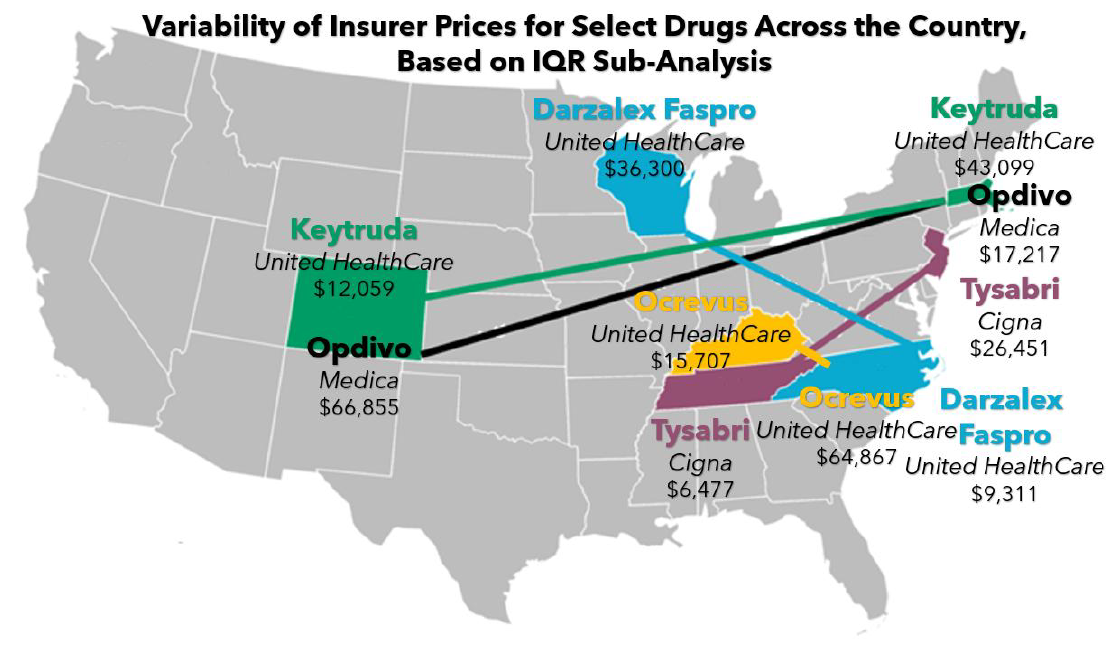

When we evaluate insurance carrier rates for these same five drugs, we see evidence of significant price variability across the country. On average, there is over a $35,000 difference in therapy cost depending upon which hospital one of these medications is received at, even if the insurance carrier managing the payment rate of the drug is fixed (Note: this result is observed within our interquartile range [IQR] sub-analysis to control for outliers). As shown below, these pricing disparities are significantly large enough to theoretically fund travel expenses between the hospitals while still resulting in significant savings. This highlights a critical reality: even with the same insurance carrier, drug prices can fluctuate dramatically from one location to another, underscoring the need for greater transparency and standardization in healthcare pricing.

The evidence suggests that while transparency requirements have unveiled price variations, they have yet to achieve meaningful price standardization, consumer usability, or systemic affordability. Ongoing challenges — such as nonstandard billing units, data entry errors, and complex contracts — hinder patients, policymakers, and purchasers in navigating and comparing hospital prices.

To explore the data that underpins the findings in this report, and to view the reported prices from more than a thousand hospitals from across the U.S., you can visit hospitaldrugprices.org.

This report underscores both the promise and limitations of current transparency policies. While federal mandates have opened a window into hospital pricing, the data remain uneven and complex, making them difficult for consumers to utilize without technical expertise. Nevertheless, these files provide a crucial foundation for understanding hospital and insurer pricing dynamics and for designing the next generation of reforms aimed at improving affordability, accountability, and equity within the U.S. healthcare system.

At 3 Axis Advisors, we understand that health care is unnecessarily complex and exceedingly expensive. With precious financial resources and the care of our loved ones on the line, we believe that through a better comprehension of our system’s mechanics and incentives, a better healthcare system is possible.

Driven by our experience, innate curiosity, and passion for finding truth, we expose and simplify inefficiencies and cost-drivers in the prescription drug supply chain and work to remedy them through data-driven research and innovative solutions.

We hope that the insights contained in this report can build upon previous drug pricing research and help to better shorten the bridge between understanding and misunderstanding the nuances of the prescription drug supply chain.

A big thanks to Patient Rights Advocate for their support and sponsorship of this important drug pricing research.

State-by-state fact sheets

Coverage

Wide disparities found in hospitals' drug prices

Axios, 3/5/26