A Model of Financial Risk to Payers from Retrospective Drug Price Concessions

Pharmacy benefit managers (PBMs) occupy a pivotal role within the United States pharmaceutical supply chain. In the U.S. prescription drug marketplace, where manufacturers and other drug channel participants frequently compete by offering rebates and other price concessions rather than by lowering list prices, among the core functions of PBMs is a central role in negotiating those discounts and concessions off list price. In this environment, PBMs use their position, leverage, and sophistication to secure lower net prices through contract negotiations with drug manufacturers and pharmacies.

Acting as intermediaries between drug manufacturers, pharmacies, and health plan sponsors, PBMs negotiate retail network pricing, administer formularies, and secure manufacturer rebates ostensibly on behalf of employers, unions, and public entities (among other activities).

This paper — conducted on behalf of the National Alliance of Healthcare Purchaser Coalitions — examines the systemic financial risk embedded in retrospective pricing and rebate guarantees that dominate pharmacy benefit manager (PBM) contracts across commercial, Medicare, and Medicaid markets. While these guarantees are marketed as cost-containment tools, their structure — rooted in benchmark discounts from Average Wholesale Price (AWP), retrospective manufacturer rebates, and affiliated group purchasing organization (GPO) arrangements — introduces significant timing, informational, and reconciliation risk to payers.

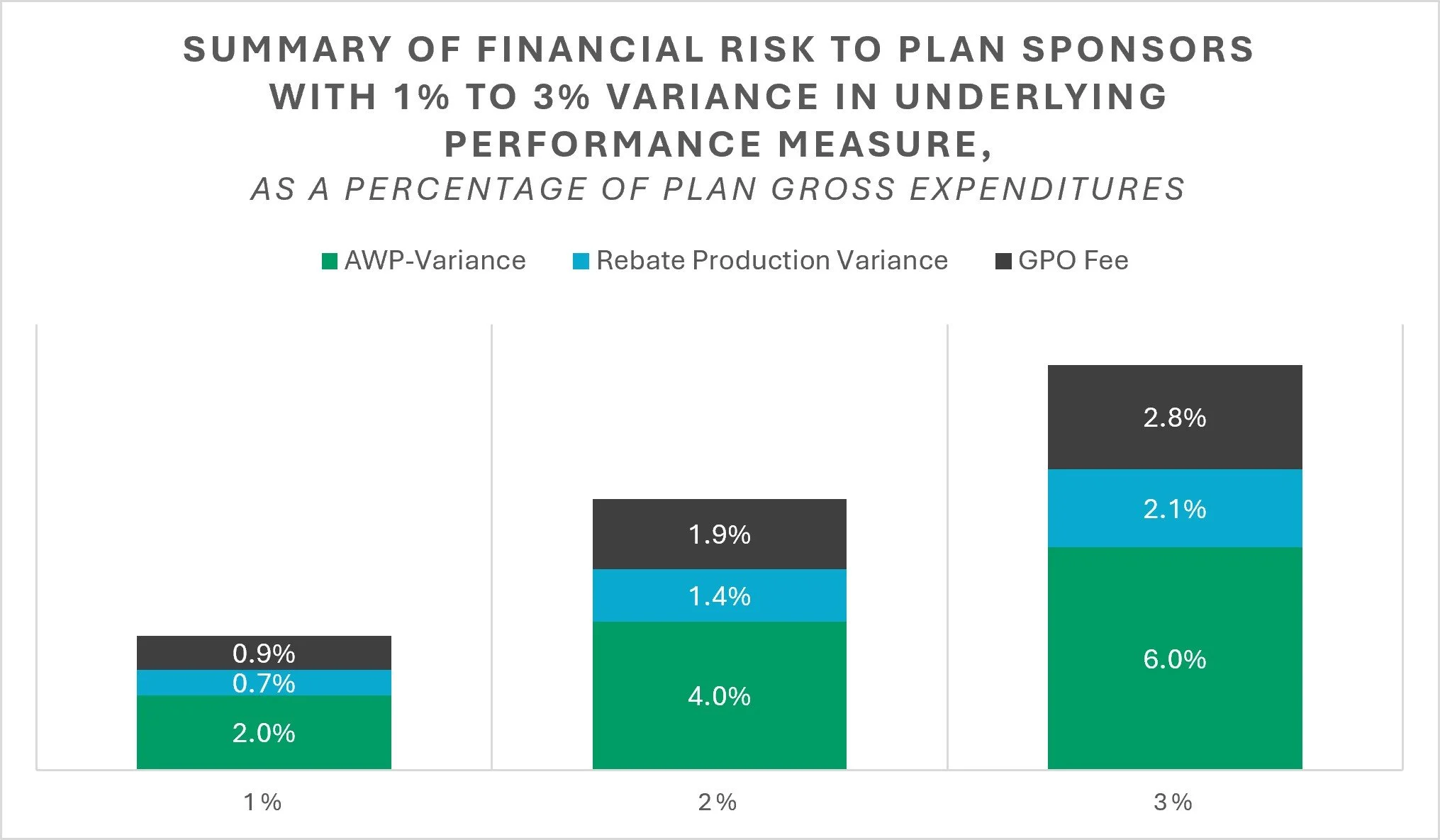

Using a model of a commercial plan with $1 million in annual drug expenditures, we quantify how small variances in benchmark pricing and rebate realization translate into material changes in net plan costs. In the modeled plan, aggregate pharmacy reimbursement equates to approximately AWP – 50%. Because this discount is reconciled retrospectively, a 1% variance in AWP performance results in roughly a 2–3% change in total plan expenditures. Similarly, rebates offset approximately 45% of gross spending in the model; a 1% shortfall in rebate realization produces an additional 2–3% increase in net costs. When potential GPO fee retention (1–3% of Wholesale Acquisition Cost [WAC]) is incorporated, total financial exposure attributable solely to retrospective reconciliation structures rises to an estimated 3–5% of annual prescription drug spending.

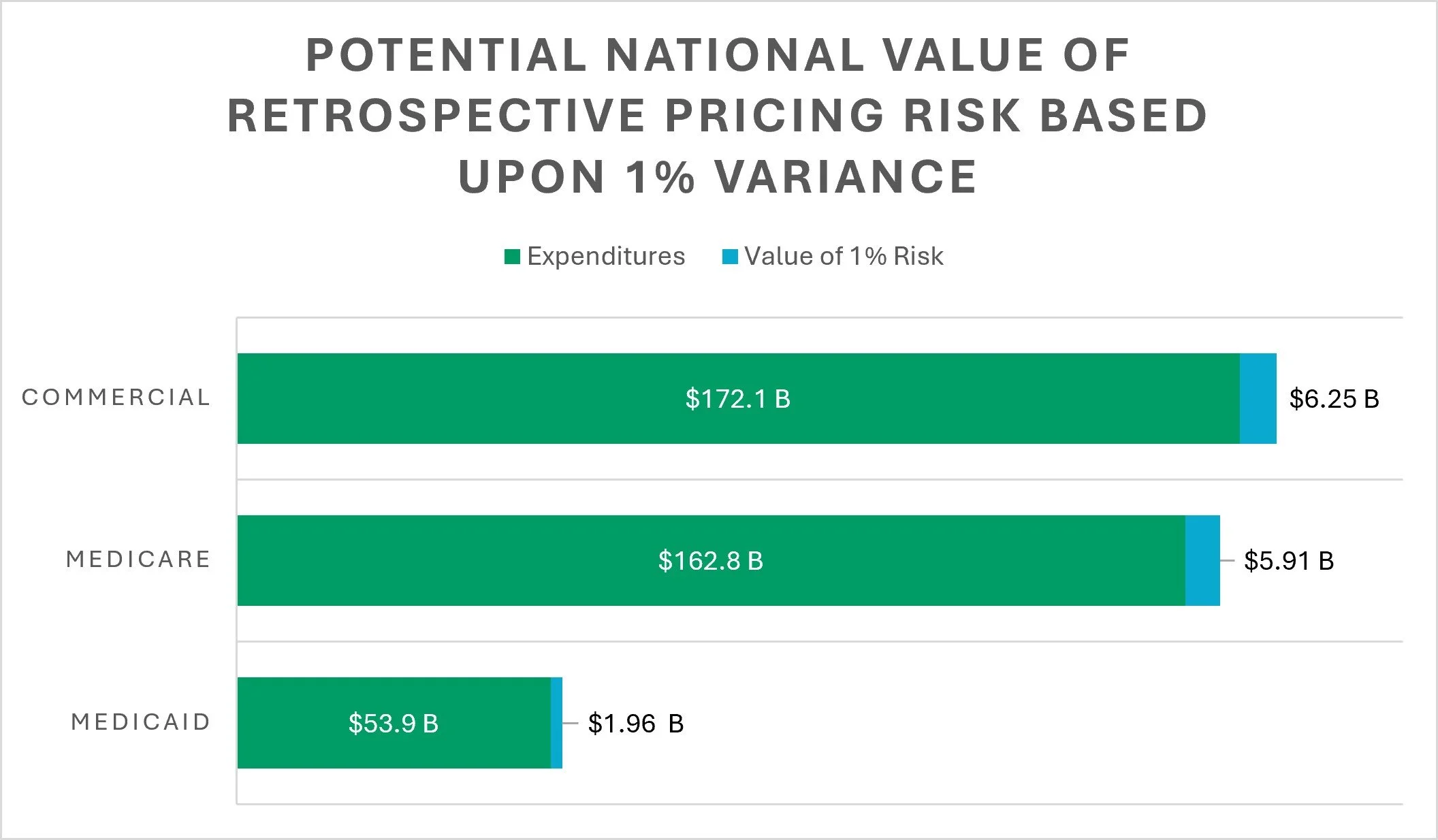

These findings align with recent federal audits of PBM-managed plans, where unremitted rebates and unpassed discounts equaled approximately 4-5% of total pharmacy expenditures. At the national level, the implications are substantial. In 2024, U.S. net prescription drug spending totaled approximately $467 billion, including $172.1 billion in private insurance, $162.8 billion in Medicare, and $53.9 billion in Medicaid. Applying a 1% variability assumption across AWP and rebate reconciliation suggests up to $14.1 billion in annual prescription drug spending is exposed to retrospective pricing risk. If exposure approaches the 4% levels observed in recent audits, the annualized financial impact could approximate $27.4 billion in the commercial market, $22.5 billion in Medicare, and $7.6 billion in Medicaid.

Collectively, the evidence demonstrates that retrospective PBM guarantees do not eliminate pricing risk — they transfer and monetize it. The timing of reconciliation, definitional flexibility, rebate exclusions (including 340B claims), and PBM GPO fee structures systematically shift financial uncertainty to payers while limiting independent verification. Transitioning toward acquisition-based reimbursement models, point-of-sale price reductions, enhanced audit rights, and shorter reconciliation cycles would materially reduce exposure and improve cost predictability across public and private programs.

This paper was begun and the analytical work was completed prior to enactment of the Consolidated Appropriations Act of 2026 (CAA), which includes significant pharmacy benefit manager (PBM) reforms, affecting commercial group health plans and Medicare Part D. The CAA expands transparency, strengthens audit rights, and in certain markets, limits compensation structures tied to drug prices. These changes are intended to reduce rebate retention and improve plan sponsor oversight.

However, the structural findings of this report remain materially valid. The financial exposure modeled herein arises primarily from the retrospective architecture of PBM guarantees, not solely from the risk of rebate withholding. When a substantial portion of drug value is realized months after the point of sale through aggregate reconciliation, plans continue to bear timing risk, benchmark variance risk, and definitional risk, even in a fully compliant regulatory environment. The mathematical sensitivity demonstrated in this analysis—where small variances in AWP or rebate realization translate into disproportionately large changes in net plan costs—persists so long as pricing remains benchmark-based and reconciled in arrears.

The CAA’s enhanced reporting requirements may improve visibility into these dynamics, and greater access to detailed claims and manufacturer remuneration data could make it easier for plan sponsors to model and verify exposure at the individual-plan level. Transparency can improve measurability and oversight, but it does not inherently eliminate the volatility embedded in discount-based pricing systems. Moreover, certain reforms, including compensation “delinking” provisions in Medicare Part D, do not automatically transform commercial PBM arrangements, meaning many employer plans may continue to operate under retrospective AWP-based guarantees unless contractually restructured.

Accordingly, while the CAA represents an important policy development, the economic framework presented in this paper remains applicable. Retrospective pricing systems continue to transfer timing and informational risk to plan sponsors unless value is recognized contemporaneously at the point of sale or through acquisition-based reimbursement models.

At 3 Axis Advisors, we understand that health care is unnecessarily complex and exceedingly expensive. With precious financial resources and the care of our loved ones on the line, we believe that through a better comprehension of our system’s mechanics and incentives, a better healthcare system is possible.

Driven by our experience, innate curiosity, and passion for finding truth, we expose and simplify inefficiencies and cost-drivers in the prescription drug supply chain and work to remedy them through data-driven research and innovative solutions.

We hope that the insights contained in this report can build upon previous drug pricing research and help to better shorten the bridge between understanding and misunderstanding the nuances of the prescription drug supply chain.

A big thanks to the National Alliance of Healthcare Purchaser Coalitions for their support and sponsorship of this important drug pricing research.